United States Gluten-free Baking Mixes Market Size and Forecast 2026–2034

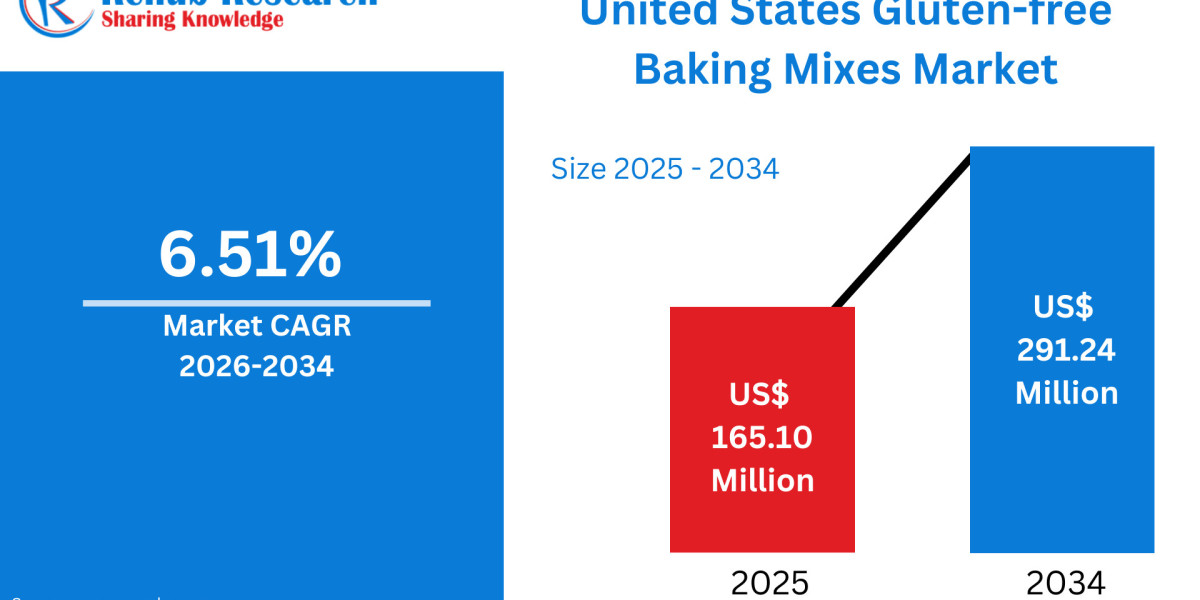

According to Renub Research United States gluten-free baking mixes market is projected to demonstrate solid and sustained growth over the forecast period, expanding from a valuation of US$ 165.10 million in 2025 to approximately US$ 291.24 million by 2034. This growth reflects a compound annual growth rate (CAGR) of 6.51% between 2026 and 2034. The market’s expansion is primarily driven by increasing awareness of celiac disease and gluten intolerance, a rapidly growing population of health-conscious consumers, and a strong shift toward clean-label and allergen-free dietary choices.

Gluten-free baking mixes have evolved from niche medical products into mainstream pantry staples across American households. Improvements in ingredient technology, flavor, texture, and nutritional performance have widened the appeal of these products well beyond consumers with diagnosed gluten sensitivities. Rising demand for convenient home-baking solutions, combined with broad availability across supermarkets, specialty stores, and online retail platforms, continues to support long-term market growth in the United States.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=united-states-gluten-free-baking-mixes-market-p.php

United States Gluten-free Baking Mixes Market Outlook

Gluten-free baking mixes are pre-blended formulations designed to replicate traditional wheat-based baking mixes while completely eliminating gluten. These mixes typically utilize alternative flours and starches such as rice flour, corn flour, almond flour, sorghum, tapioca starch, and potato starch. They are used to prepare a wide range of baked goods including bread, cakes, cookies, muffins, pancakes, brownies, and pizza crusts. By eliminating the need for complex ingredient measurement and blending, gluten-free baking mixes significantly simplify the baking process for consumers.

In the United States, the popularity of gluten-free baking mixes has surged due to heightened awareness of digestive health and food sensitivities. While celiac disease and gluten intolerance remain key drivers, an increasing number of consumers choose gluten-free products voluntarily as part of wellness-oriented lifestyles. Enhanced product quality, better textures, and improved flavor profiles have transformed gluten-free baking mixes into convenient, reliable, and widely accepted options for everyday home baking.

Increasing Prevalence of Gluten Intolerance and Health Awareness

The rising diagnosis of celiac disease, gluten sensitivity, and digestive disorders is one of the most important drivers of the U.S. gluten-free baking mixes market. Although celiac disease affects roughly 1% of the U.S. population, non-celiac gluten sensitivity impacts a significantly larger group, substantially broadening the consumer base for gluten-free baked goods. Beyond medical necessity, many consumers avoid gluten due to perceived benefits related to digestion, reduced inflammation, and overall gut health.

Gluten-free foods are increasingly associated with clean labels, fewer allergens, and improved dietary control. As awareness spreads through healthcare professionals, nutrition education, and clearer food labeling, gluten-free baking has become a normalized household activity rather than a specialized practice. Home baking allows consumers to control ingredients, sugar levels, and allergens, further fueling demand for gluten-free baking mixes across diverse demographic groups.

Home Baking Culture and Post-pandemic Lifestyle Shifts

The sustained popularity of home baking has become a powerful growth catalyst for gluten-free baking mixes in the United States. Baking is now widely viewed not only as a practical activity but also as a form of emotional wellness, creativity, and family engagement. Gluten-free baking mixes offer convenience, consistency, and reduced preparation time, making them especially attractive to consumers who may lack technical expertise in gluten-free formulations.

Busy households, working professionals, and families prefer mixes that deliver dependable results without complex sourcing of specialty ingredients. Baking also plays a significant role in households with children and special dietary needs, encouraging repeat purchases. Seasonal demand during holidays, celebrations, and family gatherings further strengthens sales cycles, ensuring stable year-round demand for gluten-free baking mixes.

Product Innovation and Premiumization Trends

Continuous product innovation is reshaping the competitive landscape of the U.S. gluten-free baking mixes market. Manufacturers are focusing on improving flavor, texture, and nutritional value to match or surpass traditional wheat-based products. Innovations include high-protein blends, incorporation of ancient grains, organic certifications, reduced sugar formulations, and allergen-free claims.

Premiumization has become a key growth strategy, with non-GMO, vegan, and functional nutrition positioning supporting higher price realization. Packaging innovations such as single-serve pouches, resealable formats, and family-size packs extend usage occasions. Brands are also expanding portfolios with specialized mixes for bread, pizza crusts, pancakes, brownies, and cakes, driving category diversification and consumer engagement.

Higher Prices and Cost Sensitivity as Market Challenges

Despite growing popularity, higher prices remain a major barrier to broader adoption of gluten-free baking mixes. Specialty raw ingredients such as rice flour, almond flour, and stabilizing gums carry higher procurement and processing costs than conventional wheat flour. Additionally, gluten-free manufacturing requires dedicated facilities, strict segregation, certification, and testing, all of which increase operating expenses.

Price sensitivity is particularly evident among middle- and lower-income households, where gluten-free purchases are often limited to medical necessity rather than lifestyle preference. Economic uncertainty further encourages value-oriented purchasing behavior. Although private-label offerings are helping to narrow the price gap, cost disparities continue to limit household penetration, repeat purchases, and overall volume growth in the U.S. market.

Texture, Taste, and Shelf-life Limitations

While formulation technology has improved substantially, gluten-free baking mixes still face challenges related to texture, taste, and shelf-life. Gluten plays a critical role in elasticity, structure, and moisture retention, making it difficult to replicate the sensory qualities of traditional baked goods. Many gluten-free products can be crumbly, dry, or lack flavor depth, negatively affecting consumer satisfaction.

Shelf-life limitations also persist due to the absence of gluten’s natural binding properties. Manufacturers must carefully balance clean-label expectations with the need for functional additives that improve performance, often at higher costs. Negative first-use experiences can discourage repeat purchases, making sensory quality a decisive factor for long-term category growth.

United States Gluten-free Bread Market

The gluten-free bread segment represents the largest and most critical category within the U.S. gluten-free baking ecosystem. Bread is a daily dietary staple, making gluten-free alternatives essential for restricted diets. Demand includes both in-store baked products and home-baked bread prepared using gluten-free baking mixes.

Consumers increasingly seek softer textures, longer freshness, and whole-grain nutritional profiles. Functional enhancements such as added fiber, protein, and probiotics support premium pricing and brand differentiation. Despite technical challenges, continuous innovation and growing consumer trust continue to drive steady volume growth in this core segment.

United States Gluten-free Cookies and Biscuits Market

Gluten-free cookies and biscuits thrive on indulgence-driven consumption and impulse buying behavior. Unlike bread, cookies are more tolerant of gluten removal, allowing manufacturers to achieve better taste and texture consistency. As a result, gluten-free cookies are widely accepted even by consumers without diagnosed gluten intolerance.

Baking mixes in this segment allow consumers to control sweetness, fat content, and ingredient quality at home. Premium flavors, seasonal variants, and chocolate-based offerings support repeat purchases and gifting demand. With rising interest in better-for-you snacks that still deliver indulgence, this segment remains one of the fastest-growing categories in the U.S. gluten-free baking market.

United States Gluten-free Corn Flour Baking Mixes Market

Corn flour baking mixes form a foundational segment of the U.S. gluten-free market due to corn’s natural gluten-free properties and strong consumer familiarity. These mixes are widely used for cornbread, muffins, pancakes, tortillas, and regional baked goods. Corn flour offers a stable structure and approachable flavor, making gluten-free baking easier for beginners.

Corn-based mixes are relatively cost-efficient compared to nut-based flours, appealing to value-oriented consumers. However, corn products can be dense or dry if poorly formulated, prompting manufacturers to enhance blends with starches and binding agents. Strong cultural acceptance and affordability ensure continued stability for this segment.

United States Gluten-free Rice Flour Baking Mixes Market

Rice flour baking mixes are favored for premium and versatile formulations due to their neutral flavor, fine texture, and high digestibility. These mixes are used across cakes, cookies, bread, waffles, and multipurpose applications. White and brown rice flours allow brands to position products in indulgent or health-focused segments.

Although rice flour requires additional starches and gums to achieve elasticity and moisture retention, it delivers predictable results that appeal to first-time gluten-free consumers. Growing demand for hypoallergenic and easily digestible ingredients supports steady expansion of this segment.

United States Gluten-free Baking Mixes Convenience Stores Market

Convenience stores represent a smaller but gradually growing distribution channel for gluten-free baking mixes. While traditionally focused on ready-to-eat products, convenience stores are allocating more shelf space to health-oriented packaged foods. Single-serve and small-pack gluten-free mixes appeal to students, travelers, and urban consumers with limited storage space.

Although SKU limitations and lower product visibility remain challenges, convenience stores play an important role in trial-based exposure and emergency purchases. As grab-and-go meal preparation trends grow, the relevance of this channel is expected to increase modestly.

United States Gluten-free Baking Mixes Online Retail Market

Online retail is the fastest-growing distribution channel for gluten-free baking mixes in the United States. E-commerce platforms offer extensive product variety, specialty formulations, bulk options, and detailed ingredient transparency. Online channels are particularly important for consumers with strict dietary needs who may lack access to certified gluten-free products locally.

Subscription services, direct-to-consumer models, and repeat delivery programs foster consistent demand. Online reviews, recipes, and digital communities further strengthen brand trust and engagement. Despite challenges related to shipping costs and freshness management, online retail will remain a dominant growth driver for the foreseeable future.

California Gluten-free Baking Mixes Market

California leads the U.S. gluten-free baking mixes market, supported by a health-centric consumer base, high disposable incomes, and a strong food innovation ecosystem. Demand for clean-label, organic, and premium gluten-free products is consistently high across the state.

Retailers aggressively stock specialty baking mixes, while numerous startups focus on sustainability and plant-based nutrition. Although competition is intense, California continues to act as a trend-setting market that shapes product development and pricing strategies nationwide.

New York Gluten-free Baking Mixes Market

New York represents a high-value, urbanized market driven by dense population, diverse dietary preferences, and strong retail infrastructure. Demand is strong for artisanal, organic, and international gluten-free baking mixes. Space-constrained urban living increases demand for compact packaging and ready-to-use blends.

High brand awareness and demand for sourcing transparency characterize this market. Despite pricing pressure from high operating costs, New York remains a key revenue generator and influencer of national gluten-free trends.

Texas Gluten-free Baking Mixes Market

Texas is a fast-growth market supported by a large population, rising health awareness, and expanding retail networks. While traditional wheat-based baking remains dominant, gluten-free adoption is increasing due to allergy awareness and lifestyle shifts.

Suburban expansion and family-oriented households drive demand for school-safe and allergy-friendly baking solutions. Price sensitivity is higher than in coastal states, making private-label gluten-free mixes particularly important for volume growth.

Arizona Gluten-free Baking Mixes Market

Arizona’s gluten-free baking mixes market benefits from steady population growth, strong wellness-oriented demographics, and year-round home cooking habits. Urban centers such as Phoenix and Tucson support demand through expanding supermarket and health food store offerings.

Retirees and medically managed diet consumers provide a stable demand base, while online retail helps bridge rural distribution gaps. Despite smaller market size, Arizona continues to record consistent growth driven by health-focused consumption patterns.

Market Segmentation Overview

The United States gluten-free baking mixes market is segmented by product type, flour type, distribution channel, and geography. Product categories include bread, cookies and biscuits, cakes and muffins, and other gluten-free bakery products such as brownies. Flour types include corn flour, rice flour, and other alternative flours. Distribution channels span supermarkets and hypermarkets, convenience stores, specialist stores, online retail, and other channels across major U.S. states.

Competitive Landscape and Company Analysis

The U.S. gluten-free baking mixes market is moderately competitive and innovation-driven. Key players are evaluated across company overview, leadership, recent developments, SWOT analysis, and revenue performance. Major companies operating in this market include General Mills Inc., Conagra Brands, Inc., Kinnikinnick Foods Inc., Williams-Sonoma Inc., Continental Mills, Inc., Partake Foods, Chebe, Naturpro, King Arthur Baking Company, Inc., and SalDoce Fine Foods. These players continue to shape market dynamics through innovation, clean-label positioning, and expanding omnichannel distribution strategies.