Market Overview:

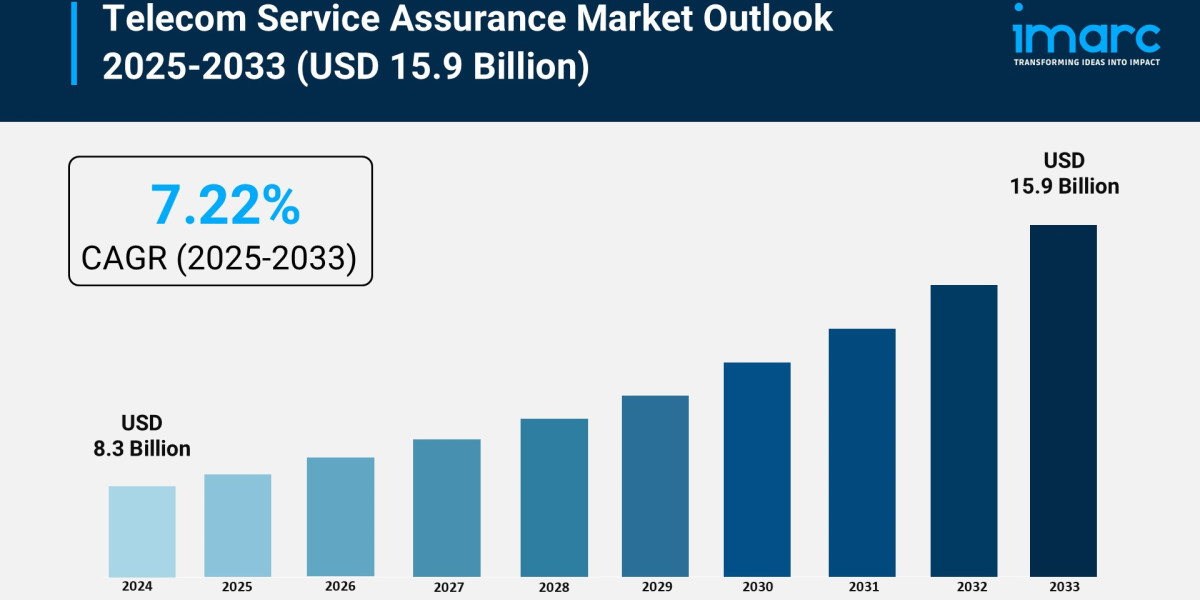

The telecom service assurance market is experiencing rapid growth, driven by global 5g and network complexity, rise of internet of things (IoT) connectivity, and regulatory and customer experience demands. According to IMARC Group's latest research publication, "Telecom Service Assurance Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033", The global telecom service assurance market size reached USD 8.3 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 15.9 Billion by 2033, exhibiting a growth rate (CAGR) of 7.22% during 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/telecom-service-assurance-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Telecom Service Assurance Market

- Global 5G and Network Complexity

The accelerated deployment of 5G networks globally is a primary catalyst for the Telecom Service Assurance (TSA) market. 5G introduces unprecedented complexity due to its use of ultra-low latency, massive machine-type communications, and network slicing, all of which demand real-time, end-to-end performance monitoring. Telecom operators worldwide are upgrading their infrastructure, evidenced by data showing that global mobile network data traffic increased significantly last year, driven in part by soaring 5G adoption. This technological leap requires sophisticated TSA solutions—such as those offered by companies like Ericsson and Amdocs—to manage the diverse, high-volume traffic and ensure the stringent Service Level Agreements (SLAs) for new 5G services are met, thereby preventing service degradation and customer churn in these intricate network architectures.

- Rise of Internet of Things (IoT) Connectivity

The proliferation of Internet of Things (IoT) devices is dramatically increasing the number of connections and the variety of services running on telecom networks, directly fueling the demand for TSA. These devices, ranging from industrial sensors and smart city infrastructure to consumer wearables, require constant, reliable connectivity and service quality. Telecom operators are facing the challenge of ensuring service integrity for billions of connected nodes, which necessitates advanced assurance tools capable of handling the disparate communication patterns of Machine-to-Machine (M2M) traffic. The rapid growth in cellular IoT connections, which are projected to overtake traditional mobile broadband connections in the coming years, showcases the need for assurance systems that can monitor these specialized IoT services and proactively manage their performance and availability.

- Regulatory and Customer Experience Demands

Increasing pressure from regulatory bodies and the growing importance of customer experience are mandating higher standards for network uptime and service quality, thus boosting the TSA market. Governments and regulatory authorities, such as the Telecom Regulatory Authority of India (TRAI), are mandating tougher service quality norms, requiring operators to rectify network outages and congestion within very short timeframes, sometimes within half an hour of occurrence. This regulatory environment compels Communications Service Providers (CSPs) to invest in sophisticated, automated service assurance platforms to comply with these strict service quality metrics. Furthermore, with the rise of digital services, customer experience has become a key differentiator, making proactive assurance a necessity for reducing trouble tickets and maintaining a satisfied subscriber base.

Key Trends in the Telecom Service Assurance Market

- AI-Centric Zero-Touch Operations (ZTO)

The move toward AI-centric Zero-Touch Operations (ZTO) represents a significant trend in the TSA market, where Artificial Intelligence (AI) and Machine Learning (ML) are deployed to achieve high levels of network autonomy. This trend focuses on automating nearly all aspects of network management, from anomaly detection to root-cause analysis and self-healing remediation. A concrete example is the use of AI-augmented telemetry streams by operators to pivot from simple threshold-based alarms to predictive analytics that preemptively identify and fix congestion or fault issues before they impact the end-user. This approach allows carriers to achieve substantial reductions in their Mean Time to Repair (MTTR) by enabling closed-loop feedback systems that can self-heal degraded network segments within seconds, moving the industry from reactive to proactive service management.

- Cloud-Native Service Assurance and Open APIs

Another key emerging trend is the shift of TSA solutions from on-premise deployments to cloud-native architectures, underpinned by open APIs for seamless integration. Telecom operators are increasingly adopting cloud-based assurance solutions to benefit from their scalability, cost-efficiency, and flexibility, which is crucial for managing the dynamic and virtualized components of 5G and edge computing. Companies are promoting solutions that leverage open architecture and standardized APIs to integrate assurance functionalities with other Operational Support Systems (OSS) and Business Support Systems (BSS). This openness is exemplified by major vendors releasing virtual tap technology to ingest high-speed traffic streams across cloudified cores, allowing for microsecond-level analytics and enabling operators to leverage advanced cloud capabilities for enhanced proactive monitoring and optimization.

- Service Assurance for Network Slicing

The commercialization of 5G Standalone (SA) has introduced network slicing, which is a major trend driving the need for slice-aware service assurance. Network slicing allows operators to create multiple isolated virtual networks on a common physical infrastructure, each tailored with specific performance metrics (like ultra-low latency for autonomous driving or high bandwidth for video streaming) for different enterprise use cases. The challenge is assuring the Service Level Agreements (SLAs) for each specific slice. Active assurance technologies, which deploy test agents across the network, are being used as a real-world application to provide real-time verification of slice performance. This ensures that a specific manufacturing facility, for instance, maintains its required private 5G network quality, making this trend critical for monetizing new B2B 5G services.

Leading Companies Operating in the Global Telecom Service Assurance Industry:

- Accenture plc

- Broadcom Inc

- Cisco Systems Inc.

- Comarch S.A.

- Ericsson Inc.

- Hewlett Packard Enterprise Development LP

- Huawei Technologies Co. Ltd.

- International Business Machine Corporation

- NETSCOUT Systems Inc.

- Nokia Oyj

- TEOCO

Telecom Service Assurance Market Report Segmentation:

By Operator:

- Fixed

- Mobile

The telecom service assurance market is primarily dominated by the fixed segment, which is driven by the need for reliable connections, especially in business.

By Solution:

- Software

- Services

Software leads the market share in telecom service assurance, fueled by the demand for real-time monitoring and improved network performance.

By Deployment:

- On-premises

- Cloud-based

On-premises solutions represent the largest segment due to their enhanced control, security, and customization capabilities preferred by organizations.

By Organization Size:

- Small and Medium-sized Enterprises

- Large Enterprises

Large enterprises account for the majority of the market share, driven by investments in managing extensive networks and adopting innovative technologies like AI and big data.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America dominates the telecom service assurance market, holding the largest share, followed by significant contributions from Asia Pacific, Europe, Latin America, and the Middle East and Africa.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302