Market Overview:

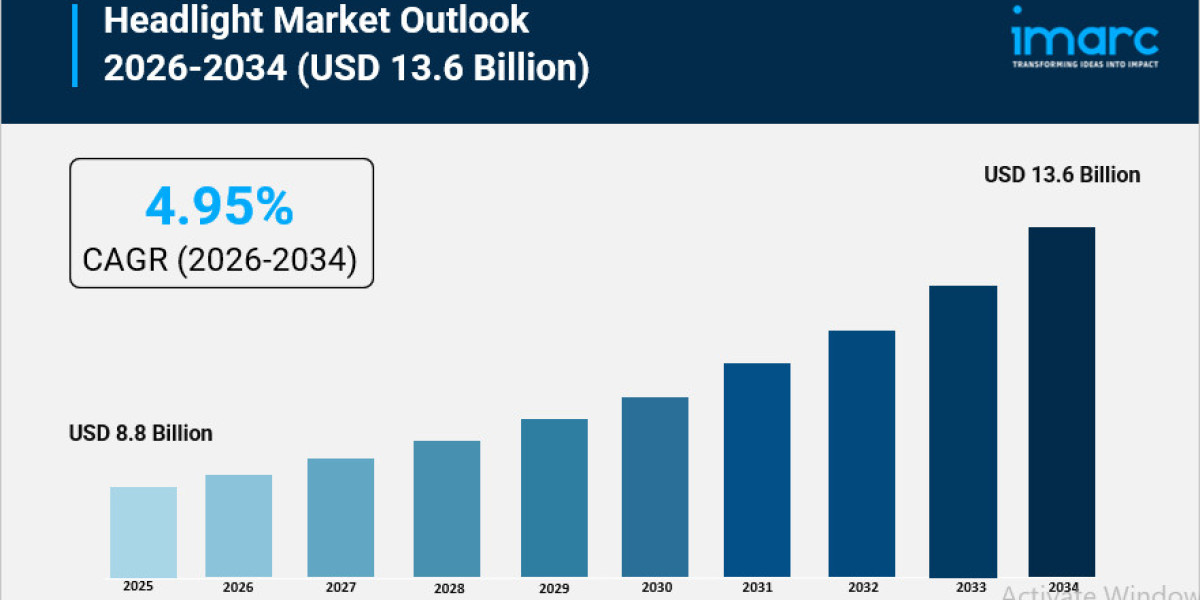

The headlight market is experiencing rapid growth, driven by acceleration of electric vehicle adoption, stringent global safety and ncap protocols, and rise of premiumization and brand differentiation. According to IMARC Group's latest research publication, "Headlight Market Size, Share, Trends and Forecast by Technology, Vehicle Type, Vehicle Propulsion, Sales Channel, and Region, 2026-2034", The global headlight market size was valued at USD 8.8 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 13.6 Billion by 2034, exhibiting a CAGR of 4.95% from 2026-2034.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/headlight-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Headlight Market

- Acceleration of Electric Vehicle Adoption

The global surge in electric vehicle (EV) production is a primary engine for headlight market growth, as these platforms prioritize energy-efficient components to maximize battery range. High-performance LED systems, which consume approximately 75% less power than traditional halogen bulbs, have become the standard for new energy vehicles. In 2025, global electric car sales reached 17 million units, significantly increasing the demand for low-wattage, high-lumen lighting modules that reduce electrical load. Major manufacturers like Tesla and BYD are integrating advanced LED projectors into their mass-market models to balance performance with weight goals. Furthermore, the high-voltage electrical architecture inherent in modern EVs allows for the seamless integration of power-intensive features like active cooling fans and sophisticated electronic control units, making EVs a natural host for next-generation lighting innovations across North American and Asian manufacturing hubs.

- Stringent Global Safety and NCAP Protocols

International regulatory frameworks and New Car Assessment Programs (NCAP) are increasingly mandating advanced lighting to reduce nighttime traffic accidents. Enhanced safety standards, such as the UN R149 regulation for adaptive driving beam systems, are compelling automakers to move beyond static lighting. In 2025, the automotive lighting market saw the exterior segment dominate with nearly 75% of the total market share, largely due to the integration of features that improve pedestrian detection. Governments in Europe and North America have updated their safety protocols to reward vehicles equipped with high-beam assist and dynamic leveling, as these technologies can reduce glare for oncoming drivers by up to 30%. This regulatory push has transformed advanced headlights from optional luxury add-ons into essential safety components for achieving five-star safety ratings, forcing a rapid phase-out of older halogen systems in favor of smarter, compliant LED architectures.

- Rise of Premiumization and Brand Differentiation

Automotive manufacturers are increasingly utilizing headlight design as a critical tool for brand identity and market positioning. Distinctive "lighting signatures," such as sequential startup animations and blade-thin daytime running lights, serve as high-visibility differentiators in a competitive landscape. In the passenger car segment, which accounts for 70% of global headlight demand, premium brands like Audi and Mercedes-Benz are leading the deployment of matrix and laser technologies to justify higher price points. Company activities currently focus on "welcome" light sequences and customizable RGB modules that appeal to the growing luxury and enthusiast markets. This trend is bolstered by a strong aftermarket sector, where consumers seek plug-and-play LED retrofits to modernize older vehicle models. With profit margins for specialized lighting components ranging between 15% and 20% for manufacturers, the industry is seeing sustained investment in design-centric R&D to meet these aesthetic demands.

Key Trends in the Headlight Market

- Integration of Adaptive Driving Beams (ADB)

Adaptive Driving Beam technology is transitioning from a premium novelty to a mainstream standard, utilizing front-facing cameras and sensors to reshape light patterns in real-time. These systems can selectively dim individual LEDs to create "shadow boxes" around oncoming vehicles while maintaining high-beam illumination on the rest of the road. Recent insights indicate that 50% of luxury vehicles in Europe now feature these smart modules, which improve nighttime visibility without blinding other drivers. In 2026, the trend is moving toward "software-defined lighting," where the headlight's behavior can be updated via over-the-air (OTA) patches. This allows manufacturers to refine beam precision or add new safety features long after the vehicle has left the showroom. Real-world applications include highway modes that automatically narrow the beam at high speeds to prevent fatigue-inducing reflections from overhead signs and road barriers.

- High-Definition Digital Light Projection

A revolutionary trend in the industry is the adoption of High-Definition (HD) matrix systems that utilize technologies like Digital Light Processing (DLP) or micro-LED arrays. These systems contain thousands of individually controllable pixels, effectively turning the headlight into a high-resolution projector. Beyond simple illumination, these headlights can project navigation arrows, lane-keep guidelines, or warning symbols for pedestrians directly onto the road surface. For example, some 2026 models are being equipped with systems capable of projecting a "virtual path" to help drivers navigate narrow construction zones at night. This convergence of lighting and vehicle intelligence serves as a critical communication interface in the emerging autonomous driving ecosystem. By projecting symbols like a crosswalk for pedestrians, the vehicle can signal its intent, bridging the communication gap between self-driving machines and human road users in complex urban environments.

- Adoption of Laser-LED Hybrid Systems

The industry is witnessing the rise of hybrid lighting systems that combine the versatility of LEDs with the extreme range of laser diodes. While LEDs handle the wide-angle, near-field illumination, laser modules are activated at higher speeds to provide a focused high-beam that can reach distances of up to 600 meters—nearly double the range of conventional LED high-beams. This technology is becoming a hallmark of high-end SUVs and performance electric vehicles, where long-distance visibility is paramount for safety. Numerical insights show that laser headlights are roughly 10 times brighter than standard LEDs while occupying significantly less space within the housing, allowing for sleeker and more aerodynamic vehicle front-ends. Manufacturers are now focusing on making these systems more cost-effective, with export-ready hybrid kits appearing in the global supply chain to cater to both the OEM and high-end aftermarket segments.

Our report provides a deep dive into the headlight market analysis, outlining the current trends, underlying market demand, and growth trajectories.

Leading Companies Operating in the Global Headlight Industry:

- Continental Aktiengesellschaft

- De Amertek Corporation

- HELLA GmbH & Co KGaA (Faurecia SE)

- Hyundai Mobis Co. Ltd. (Hyundai Motor Group)

- J.W. Speaker Corporation

- Koito Manufacturing Co. Ltd.

- Koninklijke Philips N.V.

- OSRAM GmbH (ams-OSRAM AG)

- Robert Bosch GmbH (Robert Bosch Stiftung GmbH)

- Stanley Electric Co. Ltd.

- Valeo

- ZKW Group GmbH (LG Electronics Inc.)

Headlight Market Report Segmentation:

By Technology:

- Xenon

- LED

- Halogen

LED dominates the market due to superior energy efficiency, long lifespan, instant illumination, and compact size enabling innovative vehicle designs.

By Vehicle Type:

- Passenger Cars

- Commercial Vehicles

Passenger cars represent the largest segment owing to high production volumes, consumer preferences for advanced safety features and aesthetics, and broader affordability and accessibility.

By Vehicle Propulsion:

- ICE Vehicle

- Electric Vehicle

Internal combustion engine vehicles lead the market due to established infrastructure, lower costs compared to electric vehicles, and widespread global presence across various conditions and terrains.

By Sales Channel:

- OEM

- Aftermarket

Aftermarket holds the largest share as aging vehicles require replacement headlights, offering cost-effective alternatives with wider selection and easy accessibility through multiple channels.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific enjoys the leading position owing to significant population density, strengthening economy, major manufacturing bases in China and India, and strict vehicle safety regulations.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302